Air Travel Hits 99% Of 2019 Levels Alongside Strong Air Cargo Growth

The International Air Transport Association (IATA) has released data for November 2023 air travel performance indicating that air travel demand topped 99% of 2019 levels, whilst global air cargo markets for the month saw the strongest year-on-year growth in roughly two years, up 8.3%.

Image courtesy IATA

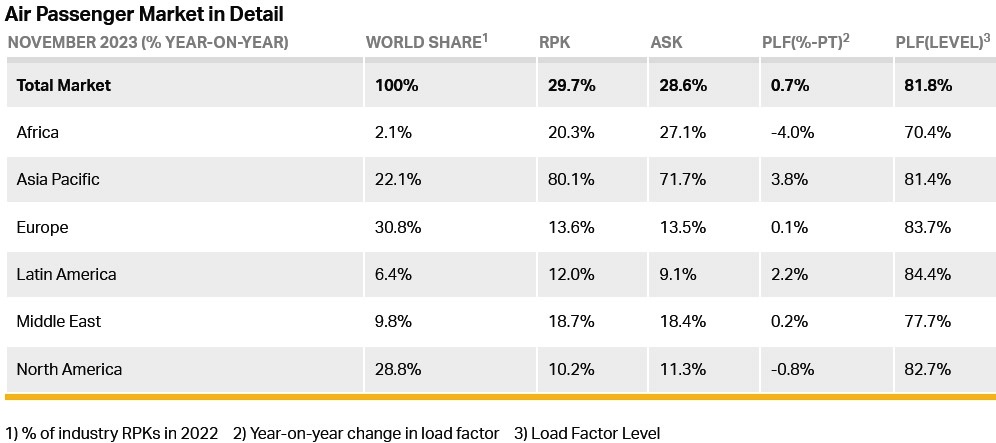

Total traffic in November 2023 (measured in revenue passenger kilometres or RPKs) rose 29.7% compared to November 2022. Globally, traffic is now at 99.1% of November 2019 levels.

International traffic rose 26.4% versus November 2022. The Asia-Pacific region continued to report the strongest year-over-year results (+63.8%) with all regions showing improvement compared to the prior year. November 2023 international RPKs reached 94.5% of November 2019 levels.

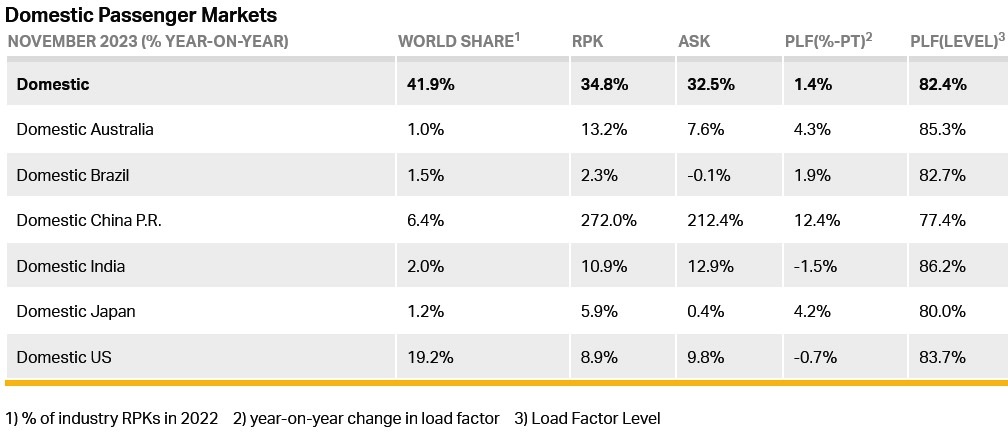

Domestic traffic for November 2023 was up 34.8% compared to November 2022. Total November 2023 domestic traffic was 6.7% above the November 2019 level. Growth was particularly strong in China (+272%) as it recovered from the COVID travel restrictions that were still in place a year ago. US domestic travel, benefitting from strong Thanksgiving holidays demand, reached a new high, expanding +9.1% over November 2019.

Willie Walsh, IATA’s Director General, said: “We are moving ever closer to surpassing the 2019 peak year for air travel. Economic headwinds are not deterring people from taking to the skies. International travel remains 5.5% below pre-pandemic levels but that gap is rapidly closing. And domestic markets have been above their pre-pandemic levels continuously since April,” said Willie Walsh, IATA’s Director General.

International Passenger Markets

Asia-Pacific airlines had a 63.8% rise in November traffic compared to November 2022, which was the strongest year-over-year rate among the regions. Capacity rose 58.0% and the load factor was up 2.9 percentage points to 82.6%.

European carriers’ November traffic climbed 14.8% versus November 2022. Capacity increased 15.2%, and load factor declined 0.3 percentage points to 83.3%.

Middle Eastern airlines saw an 18.6% traffic rise in November compared to November 2022. November capacity increased 19.0% versus the year-ago period, and load factor fell 0.2 percentage points to 77.4%.

North American carriers experienced a 14.3% traffic rise in November versus the 2022 period. Capacity increased 16.3%, and load factor fell 1.4 percentage points to 80.0%.

Latin American airlines’ November traffic rose 20.0% compared to the same month in 2022. November capacity climbed 17.7% and load factor increased 1.7 percentage points to 84.9%, the highest of any region.

African airlines had a 22.1% rise in November RPKs versus a year ago. November 2023 capacity was up 29.6% and load factor fell 4.3 percentage points to 69.7%, the lowest among regions.

Walsh said: “Aviation’s rapid recovery from COVID demonstrates just how important flying is to people and to businesses. In parallel to aviation’s recovery, governments recognised the urgency of transitioning from jet fuel to Sustainable Aviation Fuel (SAF) for aviation’s decarbonization. The Third Conference on Aviation Alternative Fuels (CAAF/3) in November saw governments agree that we should see 5% carbon savings by 2030 from SAF. This was followed up at COP28 in December where governments agreed that we need a broad transition from fossil fuels to avoid the worst effects of climate change.

"Airlines don’t need convincing. They agreed to achieve net zero carbon emissions by 2050 and every drop of SAF ever made in that effort has been bought and used. There simply is not enough SAF being produced. So we look to 2024 to be the year when governments follow-up on their own declarations and finally deliver comprehensive policy measures to incentivize the rapid scaling-up of SAF production.”

Air Cargo

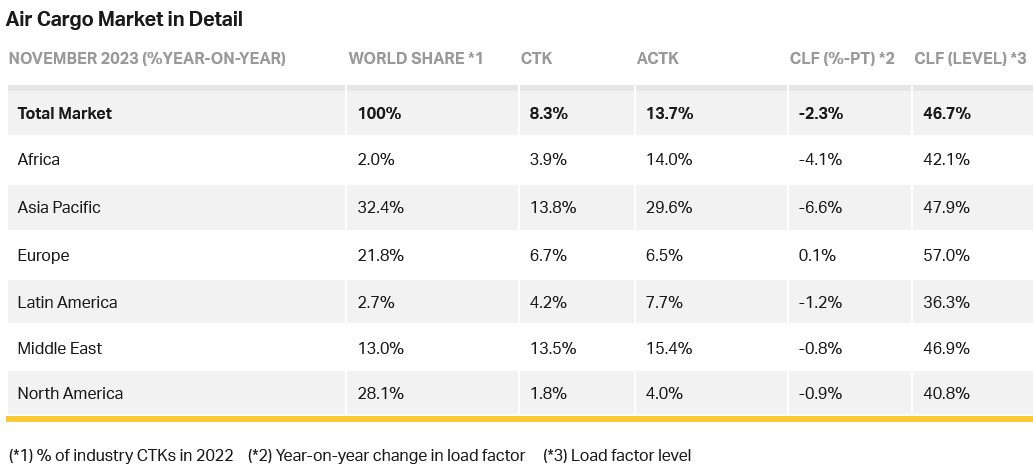

IATA data for November 2023 global air cargo markets indicates the strongest year-on-year growth in roughly two years, up by 8.3%. This is partly due to weakness in November 2022 but also reflects a fourth consecutive month of strengthening demand for air cargo.

Global demand for air cargo, measured in cargo tonne-kilometres (CTKs), increased by 8.3% compared to November 2022. For international operations, demand growth was 8.1%.

Capacity, measured in available cargo tonne-kilometres (ACTKs), was up 13.7% compared to November 2022 (+11.6% for international operations). Most of the capacity growth continues to be attributable to the increase in belly capacity as international passenger markets continue their post-COVID recovery.

Compared to November 2019 (pre-COVID-19), demand is down 2.5% while capacity is up 4.1%.

Both the manufacturing output and new export order Purchasing Managers Indexes (PMIs) – two leading indicators of global air cargo demand—continued to hover just below the 50-mark in November with small positive movements indicating a deceleration of the economic slowdown.

Global cross-border trade recorded growth for the third consecutive month in October, reversing its previous downward trend.

Inflation in major advanced economies continued to soften in November as measured by the corresponding Consumer Price Index (CPI), centring around 3% year-on-year for the United States, Japan, as well as the EU, in November. In the meantime, China exhibited negative annual growth in its CPI for the second time in a row.

Air cargo yields (including surcharges) continued their significant upward trend (+8.9% since October). Rising yields are in line with improving air cargo load factors over recent months. This could be tied in part to booming e-commerce deliveries from China to western markets.

Walsh said: “November air cargo demand was up 8.3% on 2022—the strongest year-on-year growth in almost two years. That is a doubling of October’s 3.8% increase and a fourth month of positive market development. It is shaping up to be an encouraging year-end for air cargo despite the significant economic concerns that were present throughout 2023 and continue on the horizon.”

November Regional Performance (Total Market)

Asia-Pacific airlines saw their air cargo volumes increase by 13.8% in November 2023 compared to the same month in 2022. This performance was significantly above the previous month’s growth of 7.6%. Available capacity for the region’s airlines increased by 29.6% compared to November 2022 as more belly capacity came online with the removal of COVID-19 restrictions.

North American carriers had the weakest demand growth in November with a 1.8% increase (YoY) in cargo volumes. This was, nonetheless, a significant improvement in performance compared to October’s -1.8% contraction. Capacity increased by 4.0% compared to November 2022.

European carriers saw their air cargo volumes increase by 6.7% in November compared to the same month in 2022. This was a stronger performance than in October (1.0%). Capacity increased 6.5% in November 2023 compared to 2022.

Middle Eastern carriers had the strongest performance in November 2023, with a 13.5% year-on-year increase in cargo volumes. This was similar to the significant improvement noted in the previous month’s performance (+13.0%). Capacity increased 15.4% compared to November 2022.

Latin American carriers experienced a 4.2% increase in cargo volumes compared to November 2022, very similar to the 4.0% year-on-year increase recorded for October. Capacity in November was up 7.7% compared to the same month in 2022.

African airlines saw their air cargo volumes increase by 3.9% in November 2023, slightly improved compared to October’s +2.9% growth performance. Capacity was 14.0% above November 2022 levels.

No comments for "Air Travel Hits 99% Of 2019 Levels Alongside Strong Air Cargo Growth"

Post a Comment